"Rs.1,000 investment in the Bitcoin in 2010 would have got you Rs.6.6 crore today." So its worth knowing something about it. One Bitcoin is currently equivalent to Rs.2,79,419.00 (as on 01st October 2017)

How are Bitcoins created?

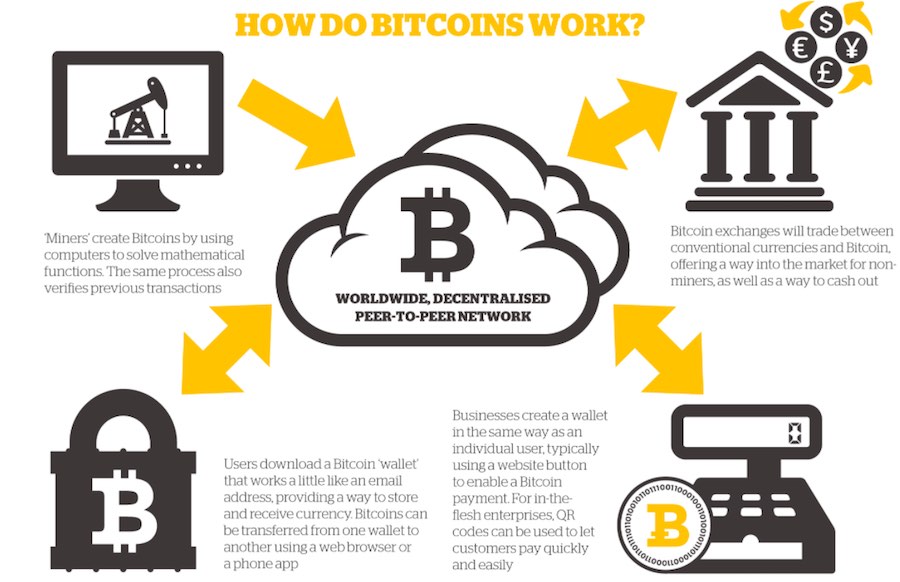

Unlike paper currencies, Bitcoins cannot be minted, instead its created digitally, by a community of people that anyone can join, who are called as miners. So, bitcoins are ‘mined’’, using computing power in a distributed network which called as the Blockchain Technology. The miners earn a reward by way of newly issued bitcoin. The pace of creation is limited, and no more than 21 million bitcoins will ever be issued. At present, only 16.8 million or 80 per cent of all the bitcoins have been mined.

What is Blockchain Technology?

The blockchain is an incorruptible digital ledger of economic transactions that can be programmed to record not just financial transactions but virtually everything of value. It’s a distributed database.

Picture a spreadsheet that is duplicated thousands of times across a network of computers. Then imagine that this network is designed to regularly update this spreadsheet and you have a basic understanding of the blockchain. Information held on a blockchain exists as a shared- and continually reconciled database. This is a way of using the network that has obvious benefits. The blockchain database isn’t stored in any single location, meaning the records it keeps are truly public and easily verifiable. No centralized version of this information exists for a hacker to corrupt. Hosted by millions of computers simultaneously, its data is accessible to anyone on the internet.

Why Bitcoin?

It's

decentralized

The bitcoin

network isn’t controlled by one central authority. Every machine that mines

bitcoin and processes transactions makes up a part of the network, and the

machines work together. That means that, in theory, one central authority can’t

tinker with monetary policy and cause a meltdown – or simply decide to take

people’s bitcoins away from them. And if some part of the network goes offline for some

reason, the money keeps on flowing.

It's easy

to set up

Conventional

banks make you jump through hoops simply to open a bank account., setting up

merchant accounts for payment. However, you can set up a bitcoin address in

seconds, no questions asked, and with no fees payable.

It's

anonymous

Well,

kind of. Users can hold multiple bitcoin addresses, and they aren’t linked to

names, addresses, or other personally identifying information.

It's

completely transparent

However,

Bitcoin stores details of every single transaction that ever happened in the

network in a huge version of a general ledger, called the blockchain.

The blockchain tells all. If you have a publicly used bitcoin address, anyone

can tell how many bitcoins are stored at that address. They just don’t know

that it’s yours. There are measures that people can take to make their

activities more opaque on the bitcoin network, though, such as not using the

same bitcoin addresses consistently, and not transferring lots of bitcoin to a

single address.

Transaction

fees are miniscule

Your

bank may charge you a £10 fee for international transfers. Bitcoin doesn’t.

It’s

fast

You can

send money anywhere and it will arrive minutes later, as soon as the bitcoin

network processes the payment.

It’s

non-repudiable

When

your bitcoins are sent, there’s no getting them back, unless the recipient

returns them to you. They’re gone forever.

Why are bitcoins popular?

Transactions can be made anonymously, making

the currency popular with speculators and criminals. Transactions and accounts

can be traced, but the account owners aren't necessarily known. However,

investigators might be able to track down the owners when bitcoins are

converted to regular currency.

Indian Senario

How to buy Bitcoins?

In

India, you can purchase Bitcoin from Zebpay exchange. Zebpay has Android and

iPhone app which lets you link your bank account for quick transfers. You can

buy Bitcoins by making a payment to Zebpay's bank account. You can also

withdraw the money to your bank account, and track data on Bitcoin valuation in

the country. Unocoin, another India-based exchange, lets you trade Bitcoins.

They can help you buy, sell, store, use and accept bitcoin.

Are Bitcoins legal in India?

India's

central bank, the Reserve bank of India or the RBI, which regulates Indian

rupee, had cautioned users, holders and traders of Virtual currencies (VCs),

including Bitcoins. The creation, trading or usage of VCs including Bitcoins,

as a medium for payment are not authorised by any central bank or monetary

authority. No regulatory approvals, registration or authorisation is stated to

have been obtained by the entities concerned for carrying on such activities. Payments

by such currencies are on a peer-to- peer basis and there is no established

framework for recourse to customer problems, disputes, etc. Legal status is

definitely not there. However, the central bank hasn't unequivocally banned

Bitcoins in the country.

Source: Internet, Compiled by Preetham Shetty and Co. Chartered Accountants

This comment has been removed by the author.

ReplyDeleteThey automatically execute and enforce the terms of an agreement when specific conditions are met.

ReplyDeleteread more

Thank you for sharing your thoughts.Discover the best ETH wallet for secure cryptocurrency storage at Droom Droom.

ReplyDeleteBest Eth Wallet

Payments transfer directly between sender and receiver without intermediaries like banks or payment processors.doberman probiv

ReplyDeleteTaxes are usually incurred later when crypto is sold and gains are realized.best solana bot

ReplyDelete